The Economy of “We’ll Figure It Out Later”

- reignitedtheseries

- May 4

- 7 min read

by Ken Oswald "__yak" Vann, Jr.

Monday, May 04, 2026

...if you're waiting on a check from Trump I wouldn't hold your breath.

People think Spirit was about a bad airline. It wasn’t. It was about a company that ran out of ways to pretend the math still worked, which is a much more uncomfortable story because it sounds a lot less like aviation and a lot more like the average American bank account.

Before my last article was even a day old, Spirit Airlines ceased operations. Not “entered a difficult quarter.” Not “announced a strategic review.” Not “tightened operations,” which is corporate for everybody "just keeping working, maybe the debt won't see us". Done. Flights canceled. Customers refunded. Crews sent home. The thing that was still technically functioning suddenly wasn’t.

And everybody treated it like something that happened overnight.

Nothing happens overnight—maybe a Rihanna pregnancy, but that's it.

Spirit hadn’t turned a profit since 2019, had already been through bankruptcy more than once, and had more than 4,000 flights scheduled through May 15 before it shut down because it didn’t have enough liquidity to keep going. That’s not a surprise collapse. That’s a long financial argument finally reaching the part where nobody can talk over the numbers anymore.

This isn’t about airlines. It’s about what happens when you keep operating like help is coming...and it doesn’t.

That’s what Spirit was doing. The merger was the bailout. The rescue deal was the bailout. The extra funding was the bailout. The next restructuring was the bailout. Something was supposed to show up and make the previous decisions look survivable.

Then it didn’t.

That’s not strategy. That’s hope with a balance sheet.

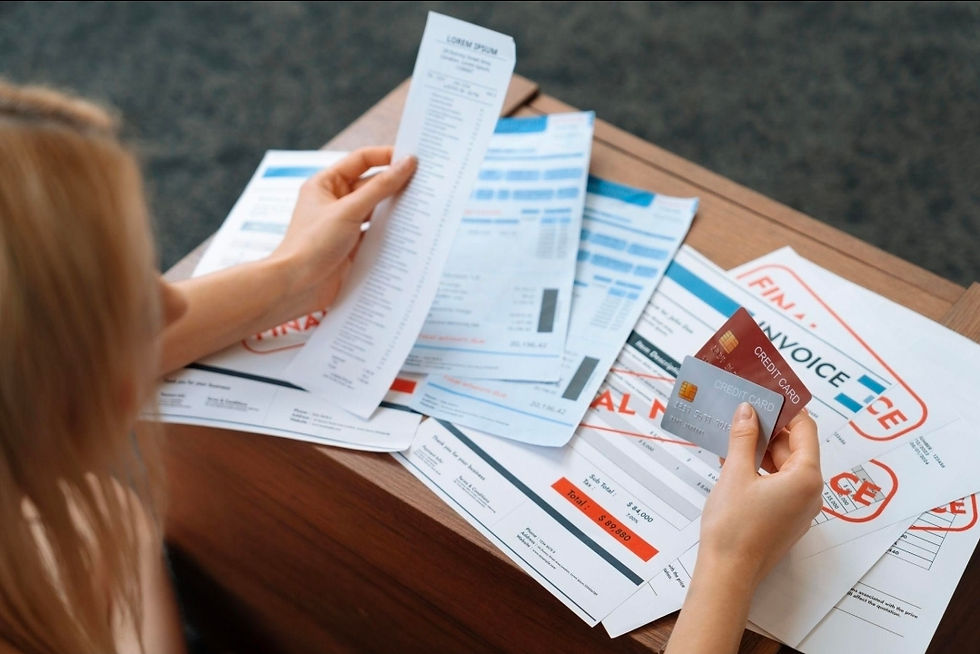

And if we’re being honest, that pattern doesn’t stop at corporations. A lot of Americans are conducting themselves the exact same way right now—not because people are stupid, not because everybody is reckless, but because the whole economy has trained people to survive by extending the problem instead of solving it. You keep the car note because maybe the next opportunity comes through. You keep the rent that’s too high because moving costs money too. You keep the credit card balance alive because something has to absorb the gap between what life costs and what income actually covers. You don’t call it a bailout, but that’s what it is in your head: some future event that shows up just in time to make the current math less insane.

A raise. A better job. A tax refund. A loan approval. Rates coming down. Debt forgiveness. Somebody finally paying what they owe you. Some invisible hand reaching into the mess and saying, “Relax, we got it from here.”

That’s the bailout mentality.

It doesn’t look like panic. It looks like holding.

That’s what makes it dangerous.

Spirit wasn’t screaming. Spirit was operating. Still selling tickets. Still flying routes. Still showing up in search results like a real option. Same way a household can look fine from the outside while everything inside is being moved around like furniture before company comes over. Minimum payment here. Extension there. Groceries on one card, gas on another, rent paid but late enough to feel it. It’s not collapse yet. It’s choreography.

But choreography is not stability—shoutout to the Jackson Family.

So now the question shifts. Not “what happened to Spirit?” We know what happened. The question is who else is waiting on relief that may not arrive.

And yes, if prediction markets let you bet cleanly on corporate collapse, people would be treating bankruptcies like player props. Lol. Don’t act brand loyal now. Half the market is already gambling on worse with less information. At least this would be based on filings.

Sleep Number

Sleep Number is the clearest name on the board because the company isn’t even hiding the distress. When a company says there is “substantial doubt” about its ability to continue as a going concern, that’s not branding. That’s not a bad headline. That is legal language doing what legal language does: saying the quiet part in the safest possible way. Sleep Number’s 2025 sales fell 16%, it posted a $132 million net loss, and then it had to amend its credit agreement with lenders, including a new $25 million term loan and covenant relief, just to give itself more room.

That’s not a turnaround yet. That’s oxygen.

And the business makes the pressure obvious. Sleep Number sells expensive comfort at a time when people are quietly cutting anything that feels optional. Nobody wants to admit they’re delaying purchases, but they are. People will sleep on a bad mattress, flip it over, throw a topper on it, blame their back pain on “getting older,” and keep moving. That’s what pressure does. It makes people negotiate with discomfort.

Revenue softens. Debt doesn’t care.

That gap just sits there, getting wider.

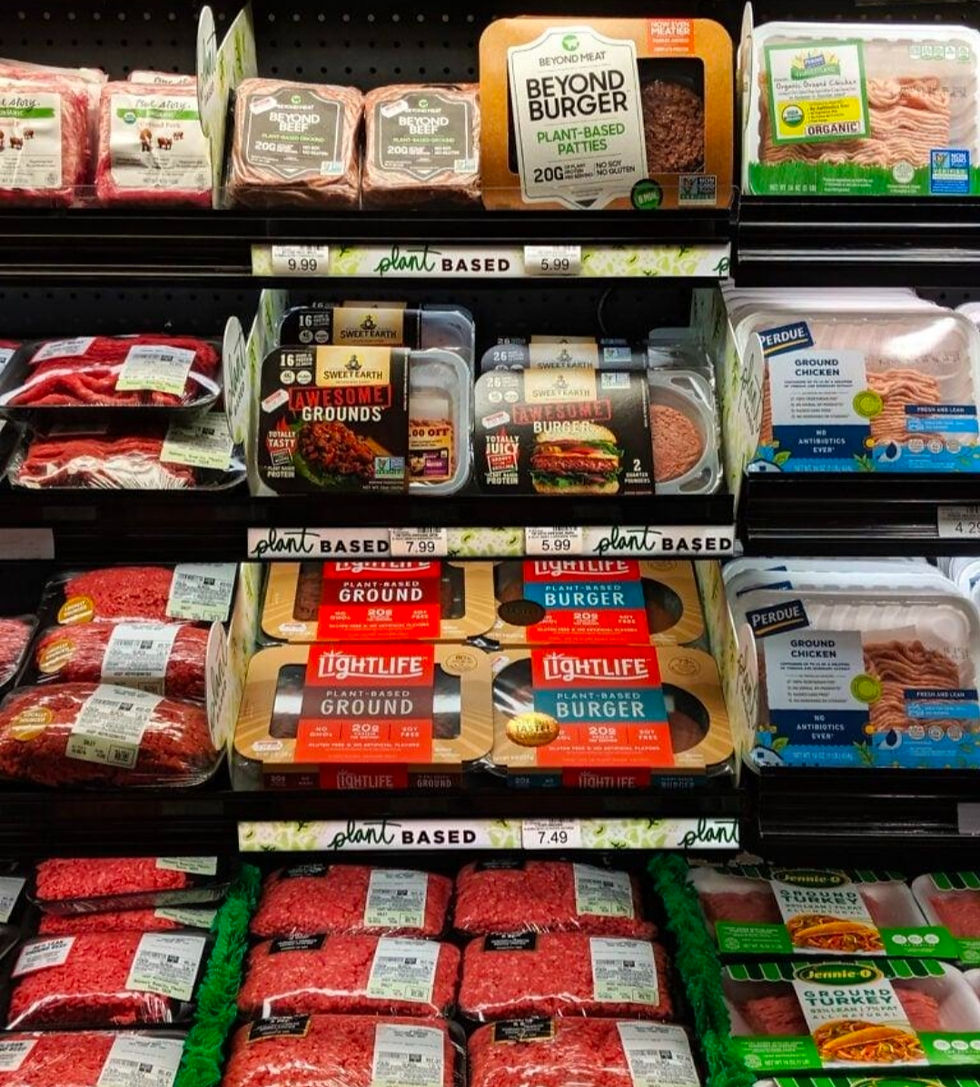

Beyond Meat

Beyond Meat is a different kind of warning because it was built on belief. For a minute, it felt inevitable—like the culture had already decided where food was going and the market just needed time to catch up. But this isn’t about what people say they support. It’s about what they repeatedly buy when nobody is watching.

That distinction matters.

Beyond Meat reported a full-year adjusted EBITDA loss of $178.4 million in 2025, and the company’s results were helped by a large non-cash gain tied to debt restructuring. It also received a Nasdaq deficiency notice after its stock traded below the minimum bid requirement.

That doesn’t mean the brand is dead tomorrow. It means the original story got too expensive to keep telling without proof. If people don’t turn the product into a habit, the company isn’t built on demand. It’s built on a memory of momentum. And memory doesn’t service debt.

Red Robin

Then there’s Red Robin, which is probably the most familiar version of the trap. Red Robin isn’t failing because nobody knows what it is. That’s actually the problem. Everybody knows what it is, and familiarity can make a brand look safer than it is.

But Red Robin lives in the middle. Not cheap enough to be the fallback. Not strong enough to be the destination. And when money tightens, people don’t make softer decisions—they make sharper ones. Fast and cheap, or intentional and worth it. “Somewhere in between” starts sounding like a luxury nobody planned for.

At the end of 2025, Red Robin had $170.2 million in outstanding borrowings under its credit facility and about $56.9 million in liquidity. Its own reporting acknowledges the pressure of variable-rate debt and refinancing exposure.

That’s not a vibes problem. That’s positioning under pressure.

And this is where the Spirit comparison becomes useful beyond Spirit. The ultra-low-cost model only works when everything behaves at the same time: fuel, labor, demand, credit, consumer tolerance. Once those variables stop cooperating, the “cheap” promise becomes expensive to maintain. Spirit was not some strange one-off failure. It was the most exposed version of a larger American habit: building entire models on thin margins and assuming the rescue comes before the math breaks.

That’s the same household problem.

If your life only works when nothing goes wrong, it doesn’t work. It’s just waiting.

That doesn’t mean everybody needs to panic. Panic is late. Panic is what happens when there’s no room left to make clean decisions. What people need right now is a colder read of their own structure. Not the moralized version, not the Dave Ramsey sermon, not the fake humble influencer budget where somebody making $300,000 tells you to meal prep and cancel Netflix. I’m talking about the real question: how much margin do you actually have if the thing you’re waiting on doesn’t happen?

Because that’s where Spirit died.

Not in the idea of the business. In the margin. In the space between what was owed, what was coming in, and what still had to be paid just to keep operating.

That’s where households break too.

So if you’re watching this correctly, you stop looking at these corporate failures like distant news. You start reading them like warnings written in a larger font. You look at your fixed costs before you look at your occasional spending. You look at the car payment, the rent, the insurance, the cards, the subscriptions stacked up like they don’t count because each one is “only” something. You stop asking whether you can technically make the payment and start asking whether the payment leaves you any room to breathe.

Because “technically current” is not the same thing as stable.

That’s the game people miss. A company can be open and unstable. A person can be paid up and unstable. A household can look normal and still be one missed check, one medical bill, one slow month, one broken transmission away from having every private problem become public at the same time.

That’s not fearmongering. That’s math.

What happens next won’t look like one big crash. It’ll look like a sequence. One company at a time. One household at a time. One “unexpected” headline after another, each one following the same pattern: pressure building, relief assumed, options narrowing, time running out.

You’ll see fewer cheap options because cheap companies are the first to break when costs rise. You’ll see higher prices because when competitors disappear, the remaining players don’t lower prices out of kindness. You’ll see more restructuring language, more emergency financing, more companies “exploring alternatives,” and more people acting shocked by outcomes that were already sitting in the numbers.

Spirit wasn’t the warning.

It was the example.

It showed us what happens when you keep moving like help is coming, then the help doesn’t come.

And once you understand that, you stop asking who’s next like it’s a guessing game. You start looking at who is still operating on hope, who is still calling delay a plan, and who has mistaken motion for stability.

That’s the whole game.

Comments